After the S&P 500’s worst first quarter on record, the stock market made history with an unprecedented recovery, taking many investors and prognosticators by surprise. Following the market lows reached on March 23rd, the S&P 500 was up 38% through the end of the 2nd quarter, marking one of the sharpest rallies over the past 100 years. The rally was not only monumental given the total return in just 3 months, but there was also 29 trading days (out of 70) that were up over 1%.

With assurance from Chairman Powell that “we will not run out ammunition”, along with optimism that coordinated and focused scientific research would eventually lead to a vaccine (WHO reported there are more than 100 vaccine candidates and over 20 in clinical trials), investors started to look past the pandemic and forward to an economic recovery.

We spent many hours at the end of 2019 looking at all the potential risks in the economy and markets and nowhere did we find a global pandemic caused by a bat in China. This quarter was the worst performing 1st quarter in history with the S&P 500 down 35% on March 23rd, before rallying to close the quarter down 20%. It took only 18 trading days to go from the greatest market in history to a bear market. There was no discrimination in the decline as nearly all companies suffered significant declines, regardless of their health and growth prospects. Unless we are going into a depression, we believe that much of the bad news has now been priced into stocks. However, a market bottom is typically a process and not an event. The coming months will tell us more about this recovery as the duration will dictate its shape: V, U or L.

As we briefly highlighted a few weeks ago, as the

equity markets began to sell-off, we continue to monitor the economic turmoil

and remain confident that global markets will recover from the economic

uncertainty that we are facing with COVID-19 (Coronavirus). As we have told

clients in the past, volatility and economic/political uncertainty is very

normal in financial markets and it’s important to not overreact and panic. It

is very normal for investors to feel like this time is different as we go

through a correction. While the circumstances driving each are always

different, one thing we know is that we eventually emerge, and over time, the

markets continue to move higher.

Of course, we are closely following all the headlines

and like everyone else don’t know how long this will persist; but what we do

know is that the underlying US economy appears strong and the financial system

is well-capitalized. We are still in the early stages of truly understanding

the full economic, financial and social impact to our economy and globally.

There is no doubt at this point that global GDP will slow, but we remind

clients that the market is forward looking and already pricing this in to some

extent. That said, the possibility of more downside is very real, and the bottoming

process may take a while.

We are closely monitoring client portfolios and will

adjust as new information becomes available, but we are not in the business of

timing markets and calling tops/bottoms. Each of our clients are allocated

based upon the plan that we set in place for them and we do not believe it’s a

time to deviate from that by either dialing up risk or by bringing it down

significantly. With the range of outcomes being so vast, we feel it best to

stay the course. It’s not time to sell but it’s also not a time to ditch your

bonds and cash for stocks.

We are hard at work trying to identify how we can use

this downturn to our advantage: tax loss harvesting, buying great companies at

steep discounts, & shedding exposure to areas of the economy that we view

as being unstable, such as Energy. You have heard us harp on the importance of

diversification and periods like we are currently experiencing are a reminder

of why it is vitally important. Our bonds and other diversifying strategies

have performed quite well over the last few weeks.

As always, we are here to answer any questions and be

a resource. Please feel free to reach out at any time.

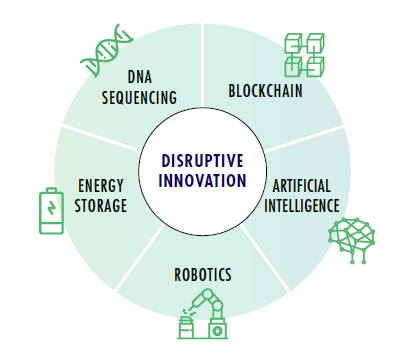

As investors continue to grapple with the near-term issues impacting global markets, we believe there is disruptive innovation happening simultaneously and could be the transformative innovation platforms that can drive the economy out of a potential recession and power growth for many years in the future. The key areas are (Source: Ark Investments):

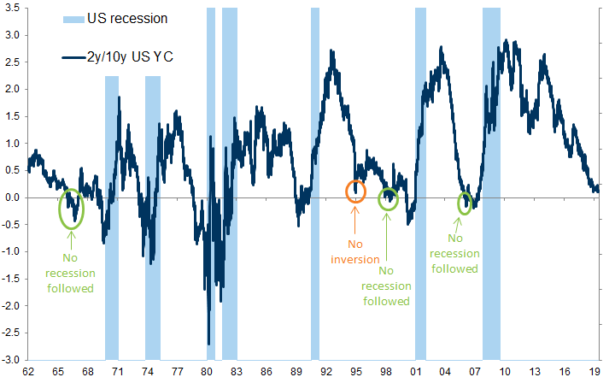

On August 14th, the 10 year Treasury Yield went slightly below the yield for the 2 year Treasury, the first time this has happened since 2007. Economist pay close attention to the 10 year vs. 2 year Treasury yields, as its historically been a strong predictor that a downturn is on the way. The yield curve has inverted before every US recession since 1955, although it sometimes happens months or years before the recession starts. The average time between the last 5 yield curve inversions and a recession was 17 months. This lead time is the key and its still very uncertain how long a lead time we may have in the current economy before there is an actual recession. That said, an inverted yield curve, like most other indicators, is not perfect and doesn’t mean a recession is imminent.

On Christmas Eve it looked like the bull market was over, with the market down nearly 20% in less than a quarter. Now, 6 months later, we are back at all-time highs and the market has rallied over 26%. While the average investor is left scratching his or her head, the rally is the result of one main catalyst, the Federal Reserve’s desire to keep interest rates low. This is not a new phenomenon, as the low interest rates have been a driver of much of the market’s success over the past decade.