In response to the COVID-19 pandemic, Treasury

Secretary Steven Mnuchin announced yesterday that individuals can defer April

15th tax payments up to $1 million, and Corporations can defer up to $10 million

of tax payments, for 90 days. Please

note that many details remain unclear with respect to this relief, and no

official written policy has been released yet, but we expect additional

guidance from the IRS in the coming days and will provide details once

available. For now, here is an overview

of what to expect:

Tax payments due April

15th can be deferred until July 15th without incurring any interest or penalties. This extension is available for all

individual taxpayers who owe < $1 million for 2019.

This 90-day extension of time to pay will likely also apply to 1st and 2nd quarter 2020 estimated tax payments due April 15th and June 15th respectively.

Mnuchin’s statement did

not extend the tax filing due date, so all taxpayers must still file their tax

returns or request extensions (Form 4868 automatically extends the filing

deadline to October 15th) by April 15th.

For anyone that

anticipates a refund for 2019 taxes, as usual we recommend you go ahead and

file by April 15th, if not sooner, to have that money refunded.

“We encourage those Americans who can file their

taxes to continue to file their taxes by April 15,” Mnuchin said,

especially encouraging people who will be getting tax refunds to do so.

“Just file your taxes,” he said, and “you will automatically not

get charged interest and penalties” on payments made within the 90-day

deferral period.

We are following the Families First Coronavirus

Response Act (FFCRA) closely, which will address relief in the form of tax

credits and/or cash payments to businesses and employees affected by COVID-19

and will send an update once there is an agreement.

For our business owners, we are also closely

monitoring federal and state incentives (including low interest loans, grants,

unemployment for employees, etc.) and will send details and guidelines once

available.

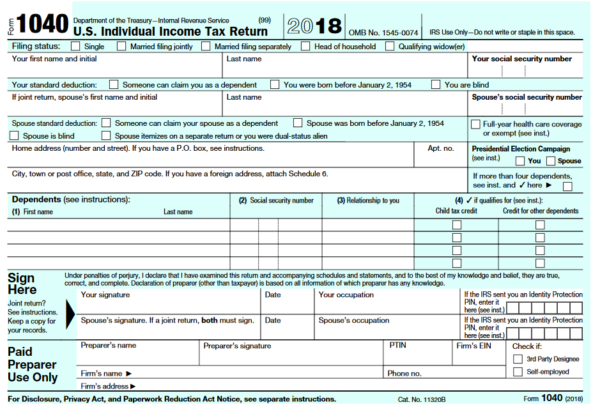

Just as the government shutdown ended, the IRS kicked-off its’ 2019 tax filing season this week on Monday, January 28th. With the window now open to file returns, we would like to draw your attention to the new postcard-sized 1040…and why it may not be as simple as it seems.

With only six weeks left in the year, we outline two planning strategies that may be relevant for you in 2018 following the 2017 Tax Cuts and Jobs Act (TCJA) – both are related to Charitable Donations and could yield significant tax savings.

Tax-Deferral Opportunity on the Sale of Low-Basis Assets:

Are you considering selling stock, real estate, or a business that has substantially appreciated in value? Are you concerned with the capital gains tax that will accompany those sales?

The December 2017 Tax Cuts and Jobs Act (TCJA) provides a new tax incentive and potential solution for investors to defer, if not eliminate, capital gains tax on the sales of assets in exchange for investments back into Qualified Opportunity Zones (“QOZs”) across the Commonwealth. Click here for more details

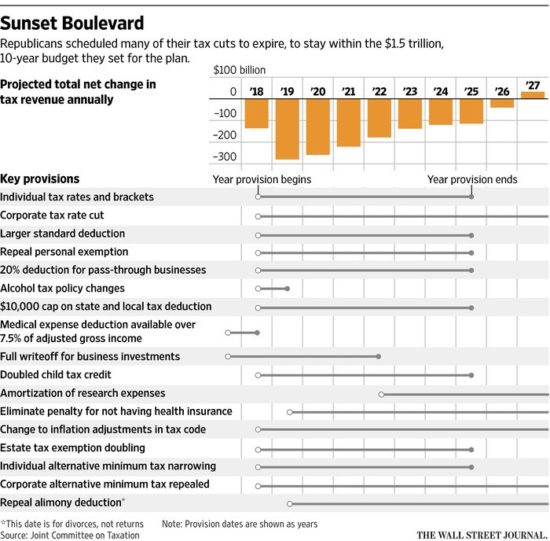

We are increasingly expectant that major tax legislation will become law as Republican leaders have indicated that after the latest round of quick negotiations, they have arrived at an agreement – the Tax Cuts and Jobs Act. We have been following the plans closely for the past year, particularly over the past three months, and continue to believe that the final version contains a host of changes that have both positive and negative impacts to middle and high-income taxpayers. We also believe that the legislation carries significantly more complexity than current rules, and look forward to discussing your situation in greater detail in the coming weeks.

In the meantime, please see below a short list of actionable items before year-end as well as a handful of key provisions that may impact you as we head into 2018.

Considerations Before Year-End 2017

Deferring Income and Accelerating Deductions: In anticipation of lower tax brackets in 2018 and more favorable corporate tax rates for many of our business-owner clients, the common strategy of deferring income into 2018 and accelerating deductions before year-end still applies (if you are in the green income brackets in the chart below). Consideration should always be given to managing tax liabilities over multiple years to avoid spikes in income and deductions that could cause you to pay tax at significantly higher rates.

State and Local Taxes: The Act will prevent many of our clients from deducting their state income taxes paid beginning in 2018 as it imposes a $10,000 cap on the combined total of property and state income taxes. As such, risking the permanent loss of this deduction going forward, we recommend all clients consider paying their entire 2017 state tax liability before December 31st, as well as real estate and personal property taxes due in early 2018.

Charitable Donations: The deduction for charitable donations will remain under the Act, however the standard deduction is scheduled to increase beginning in 2018 – from $12,700 for a married couple filing a joint return to $24,000. It is anticipated that this increased standard deduction, combined with the disallowance of deducting more than $10,000 of state and local taxes, will dramatically decrease the number of taxpayers who itemize their deductions. If you do not expect to clear the new standard deduction going forward, consider grouping two or more years of charitable contributions into a single year, then minimizing the deduction in the future. We believe that this only makes sense with existing charitable commitments, or through a Donor Advised Fund, as to not change your overall philanthropic plan.

Key Provisions of the Act

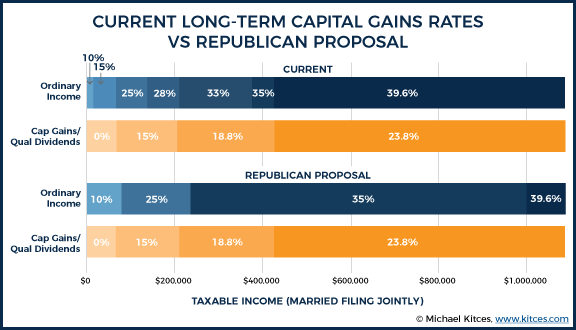

New Brackets: The top tax bracket will be reduced to 37%, down from 39.6%, and will begin at taxable income of $600,000 for a married couple filing a joint return. See comparison at right of current and proposed rates, which are generally favorable to everyone.

Expanded Standard Deduction and Repeal of Personal Exemptions: The Act consolidates and expands the Standard Deduction and Personal Exemptions into a single, larger standard deduction of $24,000 for married couples (an increase from $12,700). With the repeal of Personal Exemptions, the larger standard deduction is only slightly better than the current benefit of both Personal Exemptions and the Standard Deduction, and less favorable for some.

Business Income Tax: The most controversial of the provisions relates to the lower tax rate for some pass-through business entities, particularly when compared to the new, top corporate tax rate.

The Act calls for a reduction in the top corporate tax rate, C-corporations, from 35% to 21% and elimination of the corporate AMT.

Many pass-through businesses will receive a 20% deduction against their business income, or, in practice, their owners will be taxed on only 80% of business income. There are a number of restrictions in place intended to limit income eligible for the lower pass-through rate and “service” businesses are excluded if owner income is greater than $315,000.

For many of our clients, we see this as one of the greatest planning opportunities in the Act.

Once the Act becomes law, we plan to send a more comprehensive update outlining more provisions and planning ideas – stay tuned!

November 3, 2017: Yesterday House Republicans released details of the “Tax Cuts and Jobs Act” (link: Tax Bill). The plan calls for steep tax cuts in business tax rates, an eventual repeal of the estate tax, a reduction in the number of individual income tax brackets, elimination of the Alternative Minimum Tax, significant changes to itemized deductions and the standard deduction, as well as a host of other changes that have both positive and negative impacts to middle and high-income taxpayers.

The Tax Policy Center, a nonpartisan think tank based in Washington D.C., cites five big take-aways:

It is a tax cut, not tax reform.

It is not the biggest income tax cut in history – not even close.

For households, it will almost surely create winners and losers. Many middle-income households are likely to pay more under this plan, not less.

It is not tax simplification. Indeed, for many taxpayers the House bill would make filing more complicated

At the end of 10 years, it likely would end up increasing the deficit by far more than the advertised $1.5 trillion (TPC estimates $2.4 trillion and it will not lead to a 3 percent permanent economic growth).